How to Create Your First Budget in Less Than 15 Minutes

You do not need a perfect spreadsheet, thirty categories, or a free Saturday afternoon to start budgeting.

You need less than 15 minutes and a simple answer to one question: what should this money do before it disappears?

That is the first budget. Not the final version. Not the one you will use forever. A working version you can adjust as life happens.

The goal is momentum. Endless categorizing feels productive, but it is usually fake progress. Starting high-level gets you moving. You can get nitpicky later.

What you need before you start

Three things:

- What landed in your bank account. Open your bank account and look at the deposits from your last paycheck or last month. Use the money that really showed up.

- The bills that show up no matter what. Rent, mortgage, utilities, debt minimums, insurance, subscriptions, childcare, anything that repeats.

- A short lookback, if you are starting blind. Scroll the last week or two of transactions and notice the obvious categories. Not forever. Not as a shame exercise. Just enough to see where money is leaking.

If you have a partner, pull them in for this first pass. Even five minutes together changes the budget from “your project” to “our plan.”

That is it. You do not need a binder, a calculator, or a finance degree.

Step 1: start with the monthly picture

Most bills are monthly, so start there.

Look at what lands in your bank account in a normal month. If your income changes, use a realistic average from the last few months. Do not use the best month you have ever had. That is not a plan, that is wishful thinking with better lighting.

If you are paid weekly or biweekly, that is fine. The paychecks still matter. You are just using the monthly picture so rent, utilities, subscriptions, and debt payments all show up in the same view.

Get the number close. Round down to the nearest ten or twenty. Done.

Step 2: list the required bills

Anything you cannot skip without a phone call to a company, write it down.

- Rent or mortgage

- Utilities

- Insurance

- Minimum payments on debt

- Subscriptions you still use

- Childcare, tuition, or recurring memberships

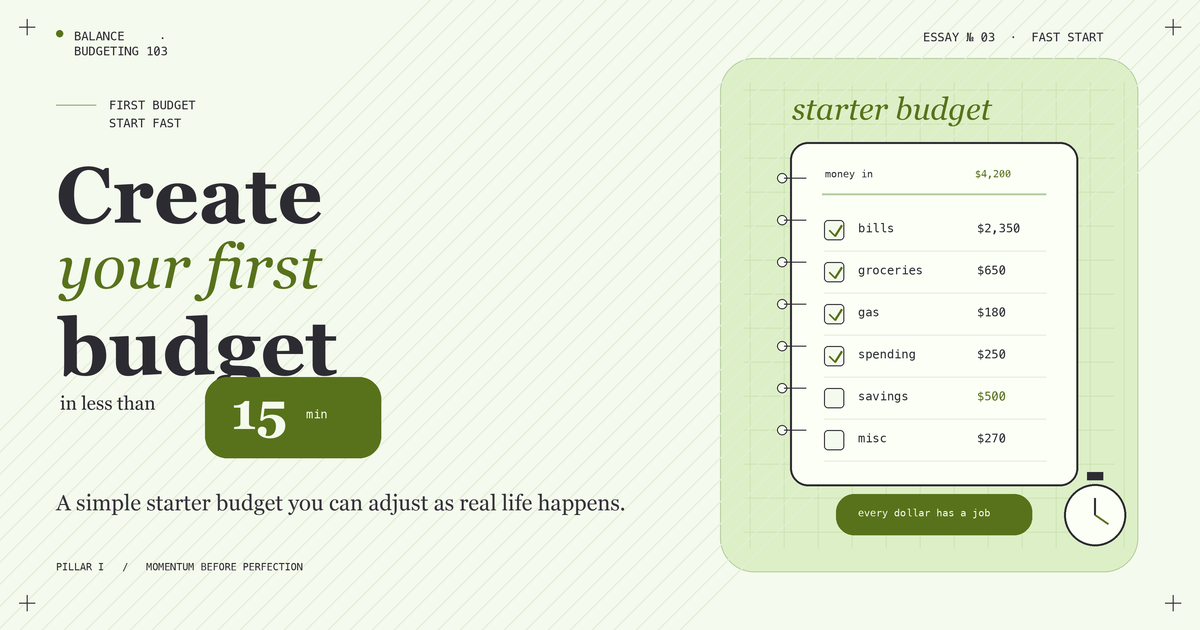

Now subtract those from the income number.

What is left is the money you can direct. Groceries, gas, eating out, personal spending, savings, misc, all of it comes from there.

If the required bills are bigger than the income, that is useful information. Not fun information, but useful. You found the pressure point in 15 minutes instead of carrying a vague money fog around for another month.

While you are here, cancel any subscription you forgot you were paying for. That counts as progress, and it feels great.

Step 3: name the categories your real life needs

Keep this high-level on purpose. Five to ten categories is enough for a first budget.

A starter set that works for most people:

- Groceries

- Eating out

- Gas or transportation

- Personal spending money, yours

- Personal spending money, your partner’s if applicable

- Kids, if applicable

- Pets, if applicable

- Savings or goal line

- Misc, for random non-recurring expenses

That is plenty.

You can split groceries into Costco, Aldi, school lunches, and “why did eggs cost that much” later if you really want to. Today, that is fake progress. Start high-level, build the right momentum, and let the categories grow with you.

The first version does not need to be perfect. It needs to exist.

Step 4: give every dollar a job before it goes

This is the move that turns the list into a budget.

Take the money left after required bills and assign it across your real-life categories before the spending happens.

Start with the categories that absolutely have to get funded: groceries, gas, the savings line that walks toward your goal. Then fund the smaller categories, including personal spending for each of you. That personal line matters. If you do not give yourself a yes line, the no lines get raided.

Keep going until the money has a job. This is zero-based budgeting in spirit, but you do not need to learn a method name to do it. The point is that the dollars are not wandering around waiting for the loudest urge to claim them.

Round numbers are fine. Rough is fine. This is a working draft.

Step 5: pick the first check-in

Before you stop, pick the next time you will look at the budget.

It can be Sunday afternoon, Saturday morning over coffee, Wednesday lunch, or while you are watching TV. Put 10 to 15 minutes on the calendar.

At the check-in, do three things:

- Look at what came in.

- Look at what went out.

- Move money between categories if life changed.

That is the rhythm. The first setup gets the budget built. The check-in keeps it useful.

And the more you do it, the faster it gets. Over time, the system starts doing more of the work for you, as long as you keep showing up.

When the plan changes

It will. That is not a problem.

Everyone has a plan until they get punched in the face. Budgeting is less dramatic than boxing, thankfully, but the idea holds. You will forget the dog’s vet appointment. Groceries might need $80 more than you guessed. A school fee will appear out of nowhere because schools are apparently powered by surprise forms.

That does not mean the budget broke. It means real life showed up, and now you have a place to respond.

Move money from a category with slack. Pull from misc if that is what it is for. If it is a true emergency, that is what the emergency fund is for.

The first month teaches you how your money behaves. The second month fits better. By the third month, you are usually adjusting instead of starting over.

That is progress.

A quick note for couples

If you have a partner, do this together the first time. Even if one of you will handle most of the maintenance later, the first build needs both names on it.

Two reasons. Categories one of you forgot get caught by the other. And it changes the budget from “the thing my partner is making me do” into “the plan we picked together.”

Pick the categories together. Pick the personal-spending number for each of you. Pick the goal line. One of you can run the check-ins later if that is how your team divides labor, but both of you need shared ownership.

FAQ

How do I start a budget?

Look at what landed in your bank account, list the bills that have to be paid, then assign what is left to the real-life categories you spend from. Keep it high-level. You can refine it later.

How long does it take to make a budget?

You can make a starter budget in less than 15 minutes. It will not be perfect, and it does not need to be. The point is to get a working version down so you can adjust it as real life gives you better information.

What are the steps to create a budget?

Five steps: find your real income, list your required bills, name your real-life categories, give every dollar a job before it goes, and pick your first check-in.

Do I need a budgeting method to start?

No. This first budget is basically zero-based budgeting without the jargon: every dollar gets a job. You can compare methods later. Today, just make the plan.

What if my income is irregular?

Use a realistic average from the last few months, or a lower month if your income swings a lot. Do not budget from your best month. Bigger months can send extra money to savings, debt, or whatever goal you are working toward.

Should every dollar have a job?

Yes, including the dollars you are saving, the dollars you are spending on yourself, and the dollars sitting in misc for random expenses. The point is that nothing is wandering around without a purpose.

What if I overspend in a category?

Move money from another category to cover it, or pull from misc if that fits. A budget is a working draft. Moving money around is the system working, not the system breaking.

Balance’s take

We built Balance because the gap between “I want to budget” and “I have a working budget” should be smaller.

Balance can help automate the first version using starter budgets based on what works for real people, not a giant blank spreadsheet. Once transactions start coming in, check-ins get faster too. Two or three minutes is enough to see where categories stand, catch anything weird, and make a quick adjustment.

The Manage page makes it easy to move money between budgets when life changes. Groceries need more? Eating out has extra? Move it and keep going. That is the whole point: the plan should adjust with you.

And if you are budgeting with a partner, you are both looking at the same plan, not two separate guesses about what was decided.

If you are ready to build your first one, start with Balance free . Less than 15 minutes from now, you can have a working budget.